A SaaS business can grow quickly and still burn cash badly. That’s the point many founders miss until a board meeting or funding process brings it into focus.

Burn multiple is one of the clearest ways to test whether your growth is efficient. It shows how much cash you’re spending to add new ARR, and investors now look at that before they get excited about headline growth.

If you’re building a UK SaaS or AI company, this metric matters. It affects runway, fundraising, and how credible your plan looks when someone starts asking harder questions.

What burn multiple actually measures

Burn multiple measures capital efficiency. In plain English, it asks a simple question: how many pounds are you burning to create £1 of new annual recurring revenue?

That matters because growth on its own can hide a lot. A company can post strong ARR growth whilst overspending on sales, paid acquisition, or headcount. Another can grow at the same pace with much less cash. Same headline. Very different business.

Burn multiple doesn’t tell you whether the business is profitable today. That’s not its job. What it does show is whether your growth model is disciplined enough to support the next stage of scale.

For founders, this is where the metric becomes useful. It forces a sharper view of how cash is being converted into recurring revenue. Not revenue in general. Not vanity pipeline. Not booked demos. New ARR that sticks.

For investors, it’s a fast read on quality. Are they looking at a business that needs constant funding support to keep moving, or one that is building real operating leverage over time?

Growth is good. Efficient growth is what gets funded.

The simple formula founders should know

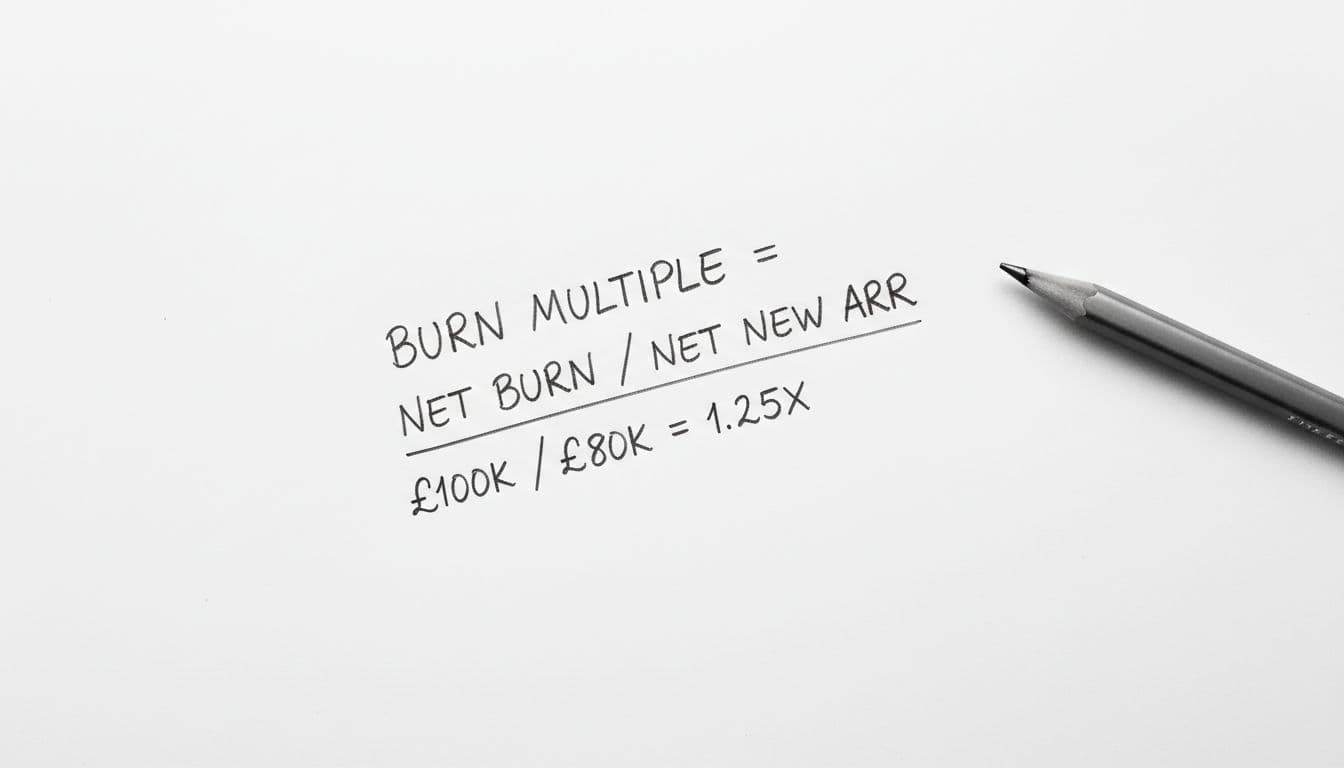

The formula is straightforward: net burn divided by net new ARR.

Net burn is the cash your business loses over a period, usually monthly or quarterly. Net new ARR is the increase in annual recurring revenue over that same period, after taking account of new sales, churn, downgrades, and expansion.

A simple example helps. If your SaaS company burns £100,000 in a quarter and adds £80,000 in net new ARR, your burn multiple is 1.25x. You’re spending £1.25 to generate £1 of new ARR.

Lower is better, up to a point. A number under 1 means the business is adding ARR with strong efficiency. A number above 2 means cash is going out faster than most investors will tolerate unless there is a clear reason.

The common mistake is to calculate it loosely. Founders often use gross new ARR, ignore churn, or mix monthly burn with annual revenue without adjusting the period. That creates a flattering number, not a useful one. If you want the metric to help decision-making, the inputs have to be clean.

Why it matters more than top-line growth alone

Top-line growth is easy to celebrate. Burn multiple is harder, because it asks whether that growth is worth what it costs.

Take two SaaS companies both adding £1 million of ARR in a year. One burns £900,000 to do it. The other burns £2.4 million. They are not performing at the same level, even if the growth chart looks similar.

This is where founder judgement comes in. If your burn multiple is poor, you don’t have a growth story. You have an expensive growth story. That changes how you hire, how long your runway lasts, and how much pressure sits on the next round.

It also changes investor confidence. Strong investors don’t want growth at any cost. They want evidence that more capital will produce repeatable, efficient growth. Burn multiple helps them test that quickly.

What a good burn multiple looks like in 2026

There isn’t one number that fits every SaaS company. Stage matters. Market matters. Growth ambition matters. AI-heavy businesses also tend to carry higher infrastructure costs, which can push burn higher in the early period.

Still, there are broad ranges founders should know in May 2026. These are not hard rules, but they are close to what investors are using as a working filter.

Benchmarks investors are likely to accept

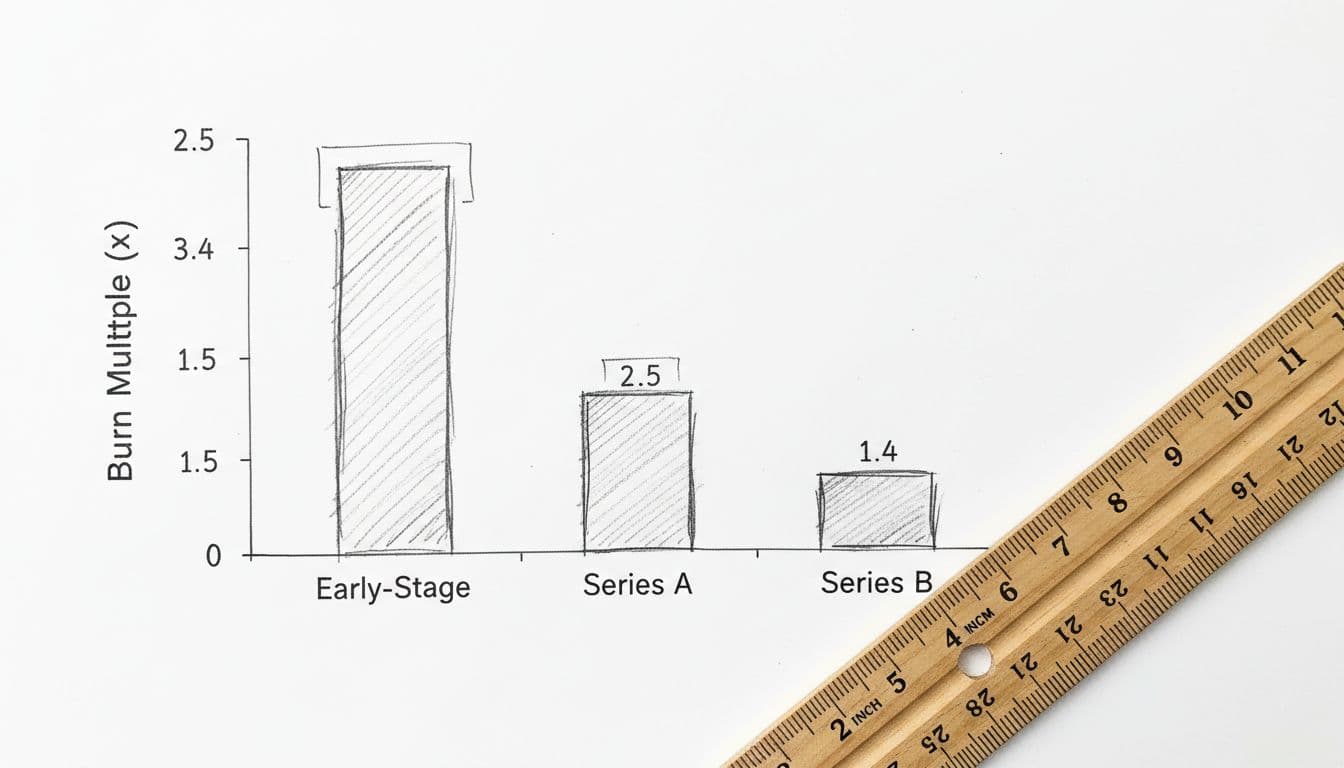

Current market ranges suggest early-stage SaaS companies often sit between 2.5x and 3.4x. Series A businesses tend to be around 1.5x to 2.5x. By Series B and later, stronger operators often move towards 1.4x or below, with the best getting under 1x.

This table gives a practical benchmark view:

| Stage | Rough 2026 range | Investor read |

|---|---|---|

| Pre-seed and seed | 2.5x to 3.4x | Understandable, but needs a route down |

| Series A | 1.5x to 2.5x | Acceptable if growth quality is strong |

| Strong growth companies | 1.0x to 1.5x | Efficient and attractive |

| Series B and later, mature scale | Below 1.0x to 1.4x | Strong capital efficiency |

| Above 2.5x at Series A+ | Over 2.5x | Usually a warning sign |

The takeaway is simple. Below 1 is usually seen as efficient. 1 to 1.5 is strong. Above 2 starts to invite tougher scrutiny, especially once you’re past seed.

When a higher number can still be tolerated

A higher burn multiple is not always fatal. Some founders are investing through a short period of acceleration, new market entry, or product expansion. That can be acceptable if the business is still proving something important and the data supports the spend.

But the days of hand-waving are over. Investors will want proof, not optimism. They will ask what is driving the burn, when it improves, and what milestones sit between today’s number and a better one.

For AI SaaS founders, this matters even more. Compute costs, model training, and technical hiring can make early burn look heavy. That can be tolerated for a period. What matters is whether those costs turn into durable revenue and whether gross margin improves as the product matures.

If the answer is vague, the higher burn multiple looks like poor control. If the answer is documented, measured, and linked to a credible plan, the conversation is different.

How investors use burn multiple during fundraising

During fundraising, burn multiple is a fast way to judge what each pound of capital is buying. It sits alongside runway, retention, growth rate, and gross margin. It is not a standalone verdict, but it carries weight because it connects spending to ARR creation.

This is why founders should know the number before the investor asks. If you can’t explain it clearly, it suggests the finance discipline behind the business is still loose.

What it says about runway and capital efficiency

A poor burn multiple shortens runway. That sounds obvious, but the second-order effect matters more. When runway tightens, options shrink. You raise under pressure, cut under pressure, and negotiate under pressure.

A strong burn multiple gives you more control. You can choose when to raise rather than when you must. You can defend your plan because the numbers show that cash is being used sensibly. That changes the tone of investor conversations.

For boards, this metric also improves clarity. It turns an abstract cash discussion into something operational. Are we spending on growth that compounds, or spending on growth that leaks out through churn, weak conversion, or low-value channels?

Why it can affect valuation and deal terms

Valuation is never based on one metric. But burn multiple shapes the confidence behind the number.

When investors see efficient growth, they are more likely to believe the model scales. That supports stronger valuations and cleaner deal discussions. It also reduces the chance of last-minute pressure to slash spend before close.

A weak burn multiple does the opposite. It raises questions about repeatability, cash discipline, and the amount of funding required before the business reaches the next milestone. That can lead to lower confidence, tighter terms, or more detailed diligence.

In practice, this is where good finance leadership matters. Founders need more than a headline metric. They need the supporting analysis, the board narrative, and a credible improvement plan.

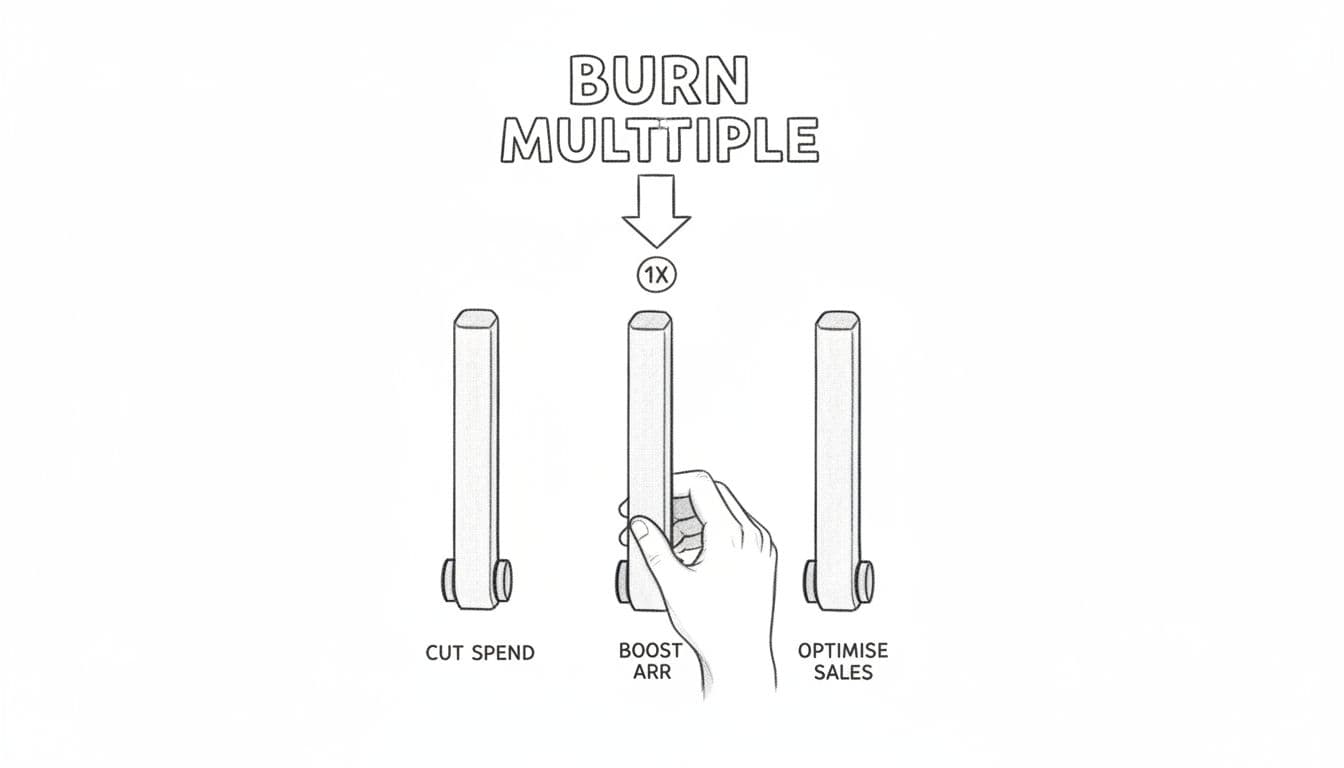

How to improve burn multiple without slowing the business

There are only two ways to improve burn multiple: reduce net burn, or increase net new ARR. The best SaaS companies do both at the same time.

That doesn’t mean panic cuts. It means disciplined allocation. Spend where revenue is proven. Fix what drags efficiency. Push harder where the model already works.

Cut spend that does not drive revenue

Start with wasted spend. Poor paid channels, overlapping tools, low-value contractors, and overhead added before it was needed all drag the number in the wrong direction.

The right question is not “what can we cut?” It is “what spend has evidence behind it?” If a channel hasn’t produced efficient pipeline in two or three cycles, stop protecting it. If a software stack is full of unused tools, clean it up. If hiring got ahead of repeatable demand, slow the pace.

This is not anti-growth. It is controlled growth. Good founders don’t cut muscle. They remove drag.

Improve pricing, retention, and expansion

Many burn multiple problems are ARR problems in disguise. If pricing is weak, churn is high, or upsell is ad hoc, net new ARR will disappoint even when gross new bookings look healthy.

Pricing often has more room than founders think. Undercharging for new tiers, AI features, service-heavy onboarding, or usage can leave revenue behind. Small changes here can lift ARR without adding much cost.

Retention usually matters even more. If customers leave six months after signing, you are paying twice for the same growth. Once to acquire them, then again to replace them. Expansion revenue helps too. Upsell and cross-sell from existing customers are often the most efficient ARR you can generate.

If customers stay longer and spend more, burn multiple improves without a major increase in cash outflow.

Make sales and marketing work harder

Sales efficiency is not only about volume. It is about fit, cycle time, conversion, and message quality.

If pipeline is full of weak-fit prospects, the business spends cash chasing revenue that doesn’t close or doesn’t stick. Better ICP definition, cleaner qualification, and sharper messaging improve conversion and reduce waste. The same budget produces more ARR.

Marketing needs the same discipline. Founders should know which channels create qualified demand, not just traffic or brand activity. Attribution doesn’t need to be perfect, but it does need to be honest. Spend where the data is repeatable. Pull back where it isn’t.

The mistakes that push burn multiple the wrong way

Most burn multiple damage does not come from one dramatic error. It usually comes from several ordinary ones, repeated for too long.

Spending before the numbers are clear

Hiring ahead of demand is one of the most common mistakes. So is scaling paid acquisition before CAC, retention, and payback are understood well enough. Founders see early momentum, then assume more spend will produce more of the same.

Sometimes it does. Often it doesn’t.

Before you push harder, the core numbers need to be credible. Which customer segment converts best? What is the payback period? Does gross margin support the model? If those answers are weak, extra spend tends to magnify the problem, not solve it.

Ignoring churn and expansion signals

Churn can sit in the background whilst headline bookings look fine. That is why it catches founders out. Net new ARR gets squeezed, burn multiple rises, and the business feels less efficient even though the team is still shipping and selling.

The fix starts with visibility. Track logo churn, revenue churn, cohort retention, and expansion by segment. If one customer group keeps leaving, don’t hide behind blended numbers. If expansion is flat, dig into activation, product value, and account management.

ARR that walks out of the front door is expensive. When customers leave as quickly as they arrive, the business is spending hard to stand still.

Conclusion

Burn multiple is one of the simplest ways to judge whether a SaaS company is growing properly. It cuts through noise and shows how efficiently cash is turning into new ARR.

For founders, that makes it useful far beyond fundraising. It should sit in your monthly reporting, your board pack, and your operating decisions. Track it regularly. Challenge it honestly. Improve it through better spend control, stronger retention, and cleaner growth execution.

If your growth story is strong, your burn multiple should be able to prove it.

Over 12 years across Big Four audit, investment banking and corporate advisory. Kishen works with UK SaaS and AI companies on financial strategy, fundraising and board-level CFO support. ICAEW regulated. Big Four trained. Based in London.